Spring statement 2018

A statement with few announcements

Aside from updated economic forecasts, the rest of the chancellor’s attention focused on policy consultations – some new, others previously announced. These consultations may feed into Autumn Budget 2018.

Chancellor Philip Hammond has delivered his Spring Statement 2018, and on his promise to move away from two major fiscal announcements every year.

There was no red briefcase, no red book, and no tax changes as the chancellor announced updated economic forecasts in a speech lasting less than half the length of any of his previous statements. Not that it comes as a surprise seeing that Hammond moved this to a Tuesday, rather than keeping it in its usual slot straight after prime minister’s questions on a Wednesday. Far from being a second financial statement of the tax year, the chancellor unveiled the latest economic forecasts alongside a raft of consultations.

The Office for Budget Responsibility (OBR) revised its forecast for growth up to 1.5% – a rise of 0.1% on the previous forecast announced in Autumn Budget 2017. However, GDP is expected to fall back to 1.3% in 2019 and 2020 as the OBR left its November 2017 forecast unchanged.

Borrowing fell to £45.2 billion in 2017/18 – £4.7 billion lower than the OBR’s forecast in November 2017, while Hammond confirmed any further borrowing is expected to fund capital investment only. Debt is also expected to start falling as a share of GDP in 2018/19, according to the OBR.

Aside from updated economic forecasts, the rest of the chancellor’s attention focused on policy consultations – some new, others previously announced. These consultations may feed into Autumn Budget 2018.

Upcoming changes

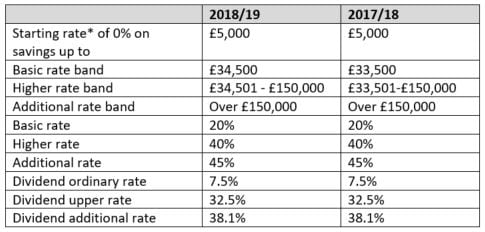

Income tax rates

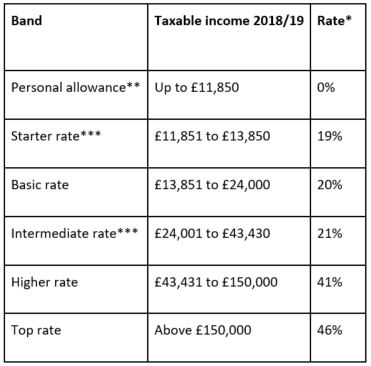

The bands and rates at which people in Scotland pay income tax have been significantly changed for 2018/19, but it will be business as usual for taxpayers in the rest of the UK.

The following income tax bands and thresholds will be in place from 6 April 2018:

Table 1 - Taxable income bands and tax rates

* The starting rate does not apply if taxable non-saving income exceeds the starting rate limit.

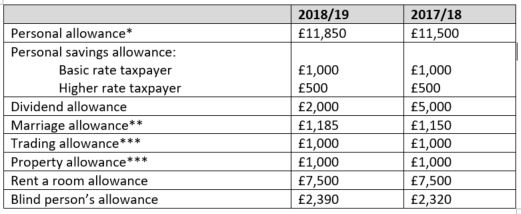

Table 2 - Allowances that reduce taxable income or are not taxable

* The personal allowance is reduced by £1 for each £2 of income from £100,000 to £123,700 (2017/18, £123,000).

** Any unused personal allowance maybe transferred to a spouse or civil partner who is not liable to higher or additional rate tax.

*** Note that landlords and traders with gross income from this source in excess of £1,000 can deduct the allowance from their gross income as an alternative to claiming expenses.

Table 3 – Scotland

*Non-savings , non-dividend rate.

**The personal allowance is reduced by £1 for each £2 of income from £100,000 to £123,700 (2017/18, £123,000).

***Indicates the two new bands being introduced.

Dividends

The tax-free dividend allowance will reduce from £5,000 to £2,000 from 6 April 2018.

Auto-enrolment

Businesses need to be aware that from 6 April 2018, the minimum employer contribution towards an employee’s workplace pension will increase from 1% to 2%.

These contributions are mandatory for workers aged between 22 and state pension age, earning more than £10,000 a year.

National living wage and national minimum wage

National minimum wage rates for all ages and apprentices are increasing from 1 April 2018.

For 18 to 20-year-olds and 21 to 24-year-olds, it will be the largest increase in a decade.

National living wages and national minimum wages rates (2018/19)

- Over-25s – £7.83

- 21-24 – £7.38

- 18-20 – £5.90

- 16-17 – £4.20

- Apprentice* – £3.70

*If under 19 or in the first year of apprenticeship.

Pensions

Pensions escaped an overhaul in Autumn Budget 2017 as the chancellor opted to leave the current system unchanged, apart from an increase to the lifetime allowance.

The lifetime allowance, which is the maximum amount an individual can draw from pensions without incurring extra tax charges, rises to £1.03 million from 6 April 2018.

ISAs

The overall annual ISA subscription limit remains at £20,000, although the Junior ISA allowance increases to £4,260 from 6 April 2018.

The £20,000 limit may also be used to invest in a Lifetime ISA, which has a maximum allowance in 2018/19 of £4,000.

Share on facebook

Share on twitter

Share on linkedin

Share on email

Share on print

Consultations

There were no tax changes and, as a result, there was a push towards dealing with potential alterations to the tax system via consultation.

Allowing entrepreneurs’ relief on gains made before dilution

It was announced that a consultation would be launched in relation to a possible change to the qualifying conditions for entrepreneurs’ relief.

In some cases, an individual may lose eligibility for entrepreneurs’ relief when their company’s fundraising efforts and strategy for growth result in their shareholding becoming diluted below 5%. This may act as a barrier to growth for some firms.

The proposals include a new process by which individuals may remain entitled to entrepreneurs’ relief on gains on shares in, or securities of, a company that relate to the time before the individual’s shareholding became diluted.

The government proposes this may be achieved through:

- allowing individuals to elect to be treated as having disposed of and reacquired their shares at the then market value

- allowing individuals to defer the taxation of this gain until an actual disposal of the shares.

Extension of security deposit legislation

At Autumn Budget 2017, the government announced it would extend existing security deposit legislation to include corporation tax and the construction industry scheme (CIS) deductions from April 2019. This consultation seeks to determine the most effective means of introducing this change.

HMRC considers most businesses meet their tax obligations and pay the right amount of tax at the right time, but a small minority choose not to pay the tax they owe or seek to unfairly reduce their tax bill. HMRC already has the power to require high-risk businesses to provide an upfront security deposit, where it believes there is a serious risk of non-payment of tax.

This approach may be taken by HMRC where a significant amount of revenue, relative to the size of the business, is at risk. For the rules to apply, there must have been a failure to comply with return filing and payments of tax, or alternatively may apply where the personnel actively involved in the current business failed to pay the taxes due in another business.

Businesses that experience genuine difficulties are not the target of any of these measures. Instead, these measures target businesses that will not, rather than cannot, pay the tax that is due.

HMRC remains committed to helping businesses which want to pay on time.

For those who are struggling, HMRC may provide a range of flexibilities, including time to pay arrangements.

Businesses with a poor compliance or payment record in relation to corporation tax or CIS may be required to make security deposits, putting additional pressure on cashflow.

Online platforms’ role in ensuring tax compliance by their users

Online platforms and marketplaces have created avenues for individuals to earn money, but they may never have earned money without an employer to act as an intermediary between them and HMRC before.

The consequences of this are that some individuals may find it difficult to understand and meet their tax obligations.

The term online platform can be quite broad but in essence will cover platforms that:

- facilitate the sharing economy, for example, by allowing people to earn money from resources they are not constantly using, such as cars or parking spaces

- assist the gig economy, for example, by allowing people to use their time and resources to generate income; or more simply

- connect buyers with individuals or businesses offering services or goods for sale.

The consultation aims to develop a better system to help these individuals comply with their tax obligations and limit opportunities for the minority who seek to avoid paying tax.

Corporate tax and the digital economy

The consultation process regarding corporate tax and the digital economy had already closed by Spring Statement 2018.

However, an updated position paper was published by the government which highlighted several key points and views from the review.

The participation and engagement of users is an important aspect of value creation for certain digital business models, and is likely to be reflected through several channels, such as the provision of content or as a contribution to certain intangibles such as brand.

The preferred and most sustainable solution to this challenge is reform of the international corporate tax framework to reflect the value of user participation.

It is important the members of the OECD’s Inclusive Framework make progress in developing multilateral solutions. To assist this process, the paper sets out some of the government’s initial considerations on what this could include.

As set out at Autumn Budget 2017, in the absence of such reform, there is a need to consider interim measures such as revenue-based taxes.

The paper explores some of the important considerations regarding the scope and design of an interim measure, and the steps that could be taken to ensure it is well targeted and protects startups and growth companies.

The government still thinks there are benefits to implementing an interim measure on a multilateral basis and it intends to work closely with the EU and international partners on this issue.

VAT, air passenger duty and tourism in Northern Ireland

Tourism makes a valuable contribution to the economy in both Northern Ireland and the rest of the UK. Concerns have been raised about the impact of VAT and air passenger duty (APD) on tourism, particularly in Northern Ireland.

The geographical situation of Northern Ireland, with a shared land border, and lower rates of VAT in the Republic of Ireland on certain tourism related items and no air travel tax (the Republic of Ireland’s equivalent of APD) are particular concerns.

The government wants further evidence to understand the concerns about the sector, that demonstrates the significance of any impacts of VAT or APD on tourism, or that helps show how VAT or APD might be used to support the growing success of tourism in Northern Ireland.

Taxation of self-funded work-related training

One focus of the government is to create a more skilled workforce, which has led to a consultation on the extension of tax relief for self-funded training by employees and the self-employed to support improving their skills and retraining.

At present, tax relief for employees or the self-employed who pay for their training can be highly restricted.

For example, a self-employed individual can normally deduct the costs of training incurred wholly and exclusively for their business where it maintains or updates existing skills, but not generally when it creates new skills.

This consultation is at an early stage and does not specify how to extend the existing scope of tax relief for self-funded work-related training.

Cash and digital payments

The review aims to find out more about removing barriers to digital payments, to better understand more about the costs and disincentives in making digital payments and what role the government can play in addressing these issues.

The government is using the consultation to determine how it can ensure cash remains accessible, especially for those groups who use cash for legitimate purposes.

Of course, the government is also seeking to determine what more can be done to clamp down on the minority who use cash to evade tax or launder money.

As part of this process, the government wishes to review large cash transactions and determine why these are used, plus assess the impact on businesses of adopting the approach taken by other countries to limit these transactions. Such impacts include the consequences for tax compliance.

Tackling the plastic problem

This consultation seeks to explore how changes to the tax system or charges could be used to reduce the amount of single-use plastics wasted by reducing unnecessary production, increasing reuse, and improving recycling. There will also be a focus on driving innovation in this area to achieve similar outcomes.

The intention is to review the whole supply chain, from production and retail, through to consumption and disposal.

Therefore, many stakeholders may have a particular interest in this consultation, as opposed to only one part of the supply chain.

Enterprise investment scheme knowledge-intensive fund consultation

The purpose of this consultation is to aid knowledge-intensive firms which have high growth potential but are research and development and capital intensive and, therefore, they may have the most difficulty obtaining the capital they need to scale up.

It attempts to review the possibility of a new enterprise investment scheme fund structure aimed at improving the supply of capital to such companies.

There is a need to build the government’s understanding of the capital gap that knowledge-intensive companies face, and the consultation seeks views on the best way of closing that gap.

Business rates

The government announced plans at Autumn Budget 2017 to reform the business rates revaluation cycle by increasing the frequency of valuations to every three years following the next revaluation.

The chancellor announced at Spring Statement 2018 that the next revaluation of business rates would be brought forward by one year to 2021, four years after the last revaluation. The aim is that ratepayers can supposedly benefit from three-year revaluations at the earliest point. It will be based on market rental values on 1 April 2019.

VAT registration threshold

The government is concerned that the current design of the VAT registration threshold may be dis-incentivising small businesses from growing their business and improving their productivity.

The chancellor has previously reported that the UK had the highest threshold in the OECD and the government had concerns about the cliff-edge nature of the threshold.

In general terms, if the taxable turnover of a business in a 12-month period exceeds the threshold (currently £85,000 until March 2020) the business must register and account for VAT.

There is growing evidence that the cliff-edge nature of the VAT threshold acts as a disincentive for small business owners who want to expand. This call for evidence and review is split into three parts:

- how the threshold might currently affect business growth

- the burdens created by the VAT regime at the point of registration, and why businesses might manage their turnover to avoid registering

- the possible policy solutions, based on international and domestic examples.

VAT collection

The government seeks to ensure a level playing field, by removing any unfair advantage overseas businesses may have over UK businesses.

HMRC estimates growth in online shopping has resulted in significant losses of VAT. It is estimated that between £1 billion and £1.5 billion was lost in 2015/16.

The government introduced packages of measures at both Budget 2016 and Autumn Budget 2017 to tackle the issue of overseas businesses selling goods to UK consumers without paying the correct UK VAT.

In March 2017, HMRC published a call for evidence, seeking views on the feasibility of a ‘split payment’ collection method for VAT as a further step in preventing this type of non-compliance.

A new consultation has been launched on VAT split payment, which seeks to determine steps that could be undertaken to allow VAT to be extracted from overseas sellers.

The thrust of the measure will be to harness new technology in the payments industry to collect VAT on online sales in real time and transfer it directly to HMRC.

There appears to be little immediate impact for businesses which conduct their trade entirely within the UK, but businesses trading internationally could face additional VAT compliance issues.

Share on facebook

Share on twitter

Share on linkedin

Share on email

Share on print

Important information

The way in which tax charges (or tax relief, as appropriate) are applied depends upon individual circumstances and may be subject to change in the future. The information in this report is based upon our understanding of the chancellor’s Spring Statement 2018, in respect of which specific implementation details may change when the final legislation and supporting documentation are published.

This document is solely for information purposes and nothing in this document is intended to constitute advice or a recommendation. You should not make any investment decisions based upon its content. ISA and pension eligibility depend on individual circumstances.

Whilst considerable care has been taken to ensure that the information contained within this document is accurate and up-to-date, no warranty is given as to the accuracy or completeness of any information.

Angela Mitchell – Partner

Angela has 19 years of experience in tax and is both a Chartered Accountant and a Chartered Tax Advisor. She is a member of the Institute of Chartered Accountants of Scotland and the Chartered Institute of Taxation. Angela is an experienced tax advisor, specialising in advising owner managed businesses and entrepreneurs on all aspects of their tax affairs including personal tax, corporate tax, capital gains tax and inheritance tax.

Donna Oswald – Partner

Donna has over 14 years experience in the field of business advisory and tax and is a member of the Institute of Chartered Accountants of Scotland. Donna qualified at a small independent firm in her home town of Perth, gaining excellent experience in all aspects of accounting, tax and bookkeeping. She passed all of her professional exams first time.